In our last installment, I concluded that the value of money appears to be destroyed faster than it is being created. I may not have made myself clear as to why this is such an alarming development.

Clearly, the creation of more money should reduce its unit value. But our normal expectation would be that if we double the amount of currency in circulation, then its unit value is reduced by half. But what happens if it falls more rapidly?

The 1923 hyperinflation in Germany is dissected in this article by Dr. H. Sennholz. According to Dr. Sennholz:

This fall in value of the total amount of currency in circulation spurred the monetary authorities in Germany to print more money. Or perhaps we should say that it provided political cover for such activities. The unit price of the mark (i.e., what one mark would buy) had fallen dramatically, but German authorities contended that it was other countries that were experiencing inflation. Germany needed to print!

Appropriately, we add the confidence ratios for Germany and Japan--at least what I have been able to glean from the World Bank. The issue of German debt was no doubt a complex one after WWII.

Both look similar. But actually the two countries are heading in different directions. The German debt has declined two of the last three reported years. Japan's debt is growing stupendously. But in both cases, the value of their gold hoards is increasing faster than their debt level.

The extreme height of the confidence ratio for Japan is a consequence of the country's comparatively small gold reserve.

On the surface, the downward sloping curve is a welcome development. It appears all four of these countries are approaching solvency. The difference is that Germany actually is becoming solvent (at least until it bails out Europe), but America, the UK, and Japan are all approaching the semblance of solvency just like your neighbour with maxed out credit cards and expenses greater than his salary who only appears to be afloat because the houses in your neighbourhood have been bid up so high (maybe you live in Vancouver).

So although technically the last three countries appear to be stumbling to some form of solvency, history informs us to be wary of surprises. Monetary authorities in Germany looked to the falling (gold) purchasing power of their total currency in circulation; Americans too should beware of authorities with their metrics and Ph.D.s telling them there is no inflation (I'm looking at you, Paul Krugman!).

Clearly, the creation of more money should reduce its unit value. But our normal expectation would be that if we double the amount of currency in circulation, then its unit value is reduced by half. But what happens if it falls more rapidly?

The 1923 hyperinflation in Germany is dissected in this article by Dr. H. Sennholz. According to Dr. Sennholz:

The reasoning that led these parties to inflate the national currency at such astronomical rates is not only interesting for economic historians, but also very revealing of the rationale for monetary destruction. The doctrines and theories that led to the German monetary destruction have since then caused destruction in many other countries. In fact, they may be at work right now all over the western world. In our judgment, four erroneous doctrines or theories guided the German monetary authorities in those baleful years.

No Inflation in Germany

The most amazing economic sophism that was advanced by eminent financiers, politicians, and economists endeavored to show that there was neither monetary nor credit inflation in Germany. These experts readily admitted that the nominal amount of paper money issued was indeed enormous. But the real value of all currency in circulation, that is, the gold value in terms of gold or goods prices, they argued, was much lower than before the war or than that of other industrial countries.

Minister of Finance and celebrated economist Helfferich repeatedly assured his nation that there was no inflation in Germany since the total value of currency in circulation, when measured in gold, was covered by the gold reserves in the Reichsbank at a much higher ratio than before the war.[2] President of the Reichsbank Havenstein categorically denied that the central bank had inflated the German currency. He was convinced that it followed a restrictive policy since its portfolio was worth, in gold marks, less than half its 1913 holdings.

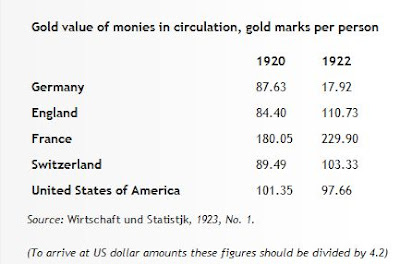

Professor Julius Wolf wrote in the summer of 1922: "In proportion to the need, less money circulates in Germany now than before the war. This statement may cause surprise, but it is correct. The circulation is now 15–20 times that of pre-war days, whilst prices have risen 40–50times." Similarly Professor Elster reassured his people that "however enormous may be the apparent rise in the circulation in 1922, actually the figures show a decline."The chart that backed up these amazing conclusions.

The Statistical Bureau of the German government even calculated the real values of the per capita circulation in various countries. It, too, concluded that there was a shortage of currency in Germany, but a great deal of inflation abroad.

From Sennholz (2006).

This fall in value of the total amount of currency in circulation spurred the monetary authorities in Germany to print more money. Or perhaps we should say that it provided political cover for such activities. The unit price of the mark (i.e., what one mark would buy) had fallen dramatically, but German authorities contended that it was other countries that were experiencing inflation. Germany needed to print!

Appropriately, we add the confidence ratios for Germany and Japan--at least what I have been able to glean from the World Bank. The issue of German debt was no doubt a complex one after WWII.

Both look similar. But actually the two countries are heading in different directions. The German debt has declined two of the last three reported years. Japan's debt is growing stupendously. But in both cases, the value of their gold hoards is increasing faster than their debt level.

The extreme height of the confidence ratio for Japan is a consequence of the country's comparatively small gold reserve.

On the surface, the downward sloping curve is a welcome development. It appears all four of these countries are approaching solvency. The difference is that Germany actually is becoming solvent (at least until it bails out Europe), but America, the UK, and Japan are all approaching the semblance of solvency just like your neighbour with maxed out credit cards and expenses greater than his salary who only appears to be afloat because the houses in your neighbourhood have been bid up so high (maybe you live in Vancouver).

So although technically the last three countries appear to be stumbling to some form of solvency, history informs us to be wary of surprises. Monetary authorities in Germany looked to the falling (gold) purchasing power of their total currency in circulation; Americans too should beware of authorities with their metrics and Ph.D.s telling them there is no inflation (I'm looking at you, Paul Krugman!).

No comments:

Post a Comment